Cash Flow Management Examples for Small Business Owners

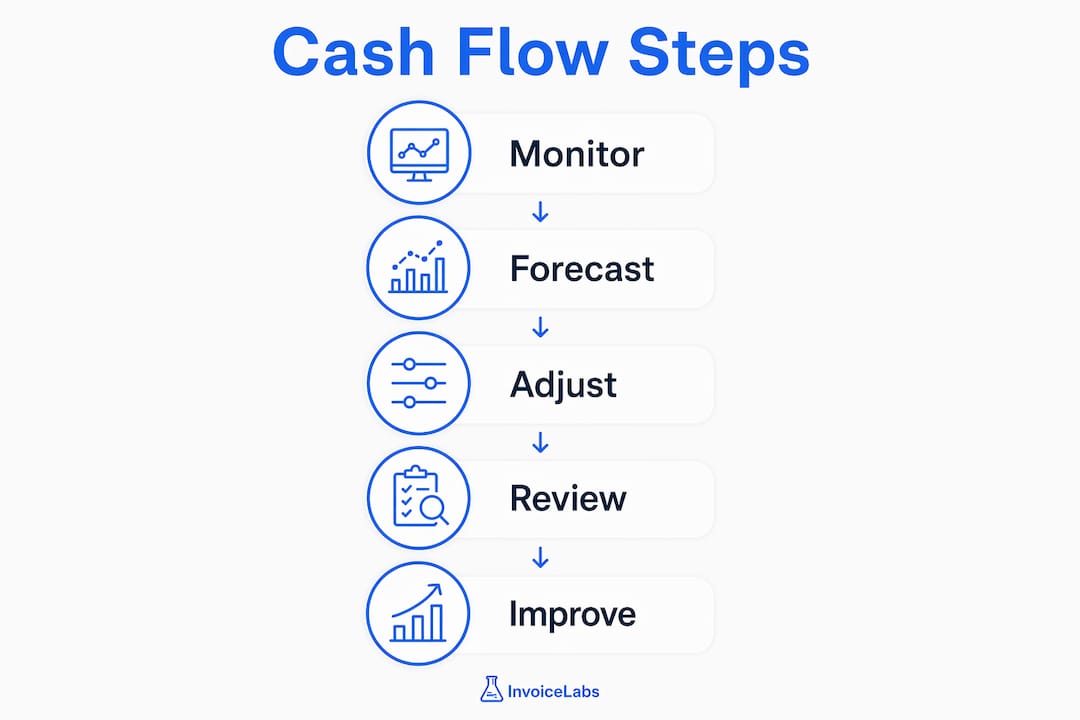

Cash flow management is the active process of monitoring, analyzing, and adjusting the movement of cash into and out of your business to maintain liquidity at all times. Unlike profitability, which measures accounting earnings, cash flow determines whether you can pay your bills next Friday. 82% of small business failures trace back to poor cash flow management, not a lack of profit. That single statistic reframes the entire conversation: a business can be profitable on paper and still collapse. This article walks through a practical cash flow management example at each stage, from core metrics to a 13-week rolling forecast, so you can build a system that actually holds.

What is a cash flow management example in practice?

A cash flow management example is any real scenario where a business owner tracks, forecasts, and adjusts cash inflows and outflows to stay solvent and fund operations. The formal industry term for this discipline is liquidity management, though most small business owners and financial advisors use “cash flow management” interchangeably. Understanding both terms helps you communicate with lenders, accountants, and CFO-level advisors.

The best single metric for measuring cash health is the cash conversion cycle, or CCC. The formula is: Days Sales Outstanding (DSO) + Days Inventory Outstanding (DIO) minus Days Payable Outstanding (DPO). A lower CCC means your business converts work into cash faster. Industry benchmarks vary widely: retail businesses often target a CCC under 30 days, while professional services firms can run negative CCCs by collecting deposits before delivering work.

The financial impact of improving your CCC is concrete. Every 5-day reduction in CCC on a $5 million revenue business frees approximately $68,000 in cash permanently. That is not a loan or a line of credit. It is real, recurring liquidity created by process improvement alone.

Working capital, calculated as current assets minus current liabilities, tells you how much cushion you have at any moment. Protecting that cushion requires discipline around cash reserves. The standard benchmark for most small businesses is 8 weeks of fixed operating expenses held in reserve. Seasonal businesses need 12–16 weeks. These thresholds are not suggestions. Dropping below your cash floor triggers a hierarchy of corrective actions, from cutting discretionary spending to drawing on a credit line.

Segmenting cash into separate buckets for operations, taxes, and contingencies prevents one of the most common small business mistakes: spending money that was already spoken for. A freelance designer who keeps all revenue in one account often pays a tax bill with cash she needed for payroll. Three accounts, clearly labeled, solve that problem structurally.

Pro Tip: Open a dedicated tax reserve account and transfer a fixed percentage of every payment received the same day it arrives. Automate the transfer so it requires no willpower.

How to build a 13-week rolling cash flow forecast

A 13-week rolling forecast updated weekly is the most useful tool for predicting and planning around cash shortages. The 13-week window is long enough to spot problems early and short enough to remain accurate. Annual forecasts are too vague for day-to-day decisions. Monthly forecasts miss intra-month timing gaps. Thirteen weeks hits the practical sweet spot.

Building the forecast: a step-by-step example

-

List all expected cash inflows. Pull your accounts receivable aging report and assign expected payment dates by customer. Add confirmed sales from your pipeline with realistic close probabilities. A consulting firm with three clients on Net-30 terms and two proposals at 70% probability can build a credible inflow schedule for the next quarter.

-

List all expected cash outflows. Include payroll dates, vendor payment due dates, rent, software subscriptions, loan payments, estimated tax installments, and owner draws. Group them by week, not by month.

-

Calculate the weekly net cash position. Subtract outflows from inflows for each week. Carry the ending balance forward as the opening balance for the next week. This running total shows exactly when your balance dips and by how much.

-

Build three scenarios. A base case uses your most likely assumptions. A downside case assumes your two largest clients pay 15 days late. A crisis case assumes one major client does not pay at all for 60 days. Running all three takes less than an hour and reveals which weeks are genuinely fragile.

-

Update every week and compare actuals to forecast. A disciplined weekly 30-minute review of actuals versus forecast catches shortfalls 60–90 days before they become emergencies. That lead time is the difference between a calm conversation with your bank and a desperate scramble for cash.

The variance analysis step is where most small business owners stop short. When actual cash is lower than forecast, the question is not just “what happened?” It is “which assumption was wrong, and does that change the next 8 weeks?” Updating your assumptions weekly makes the forecast more accurate over time.

Pro Tip: Color-code your weekly net cash rows: green for balances above your 8-week reserve floor, yellow for 4–8 weeks, and red for below 4 weeks. You will spot problems at a glance without reading every number.

What cash flow strategies can you implement immediately?

Improving your cash position does not always require new financing. Most small businesses have significant cash tied up in slow invoicing, loose vendor terms, and excess inventory. The following strategies address each of those areas directly.

Tighten invoicing and collections

Invoice immediately upon delivery and shorten your payment terms. Moving from Net-30 to Net-15 cuts your average Days Sales Outstanding nearly in half on compliant clients. Offer a 1–2% early payment discount for clients who pay within 7 days. For many clients, a small discount is worth the administrative simplicity of clearing invoices fast. For you, the cost of the discount is far lower than the cost of a short-term loan to cover the same gap.

Send invoices the same day you complete work, not at the end of the month. A freelancer who batches invoices on the last Friday of the month adds up to 30 days of unnecessary delay to every payment cycle. That delay compounds across every client and every month.

Manage payables strategically

Negotiate longer payment terms with suppliers, moving from Net-30 to Net-45 or Net-60 where possible. Most vendors will agree to extended terms for reliable, long-term customers. You do not need to ask for a discount. You are simply asking to pay on day 45 instead of day 30. That 15-day extension on a $20,000 monthly supply bill keeps an extra $10,000 in your account for two additional weeks each month.

Pay vendors strategically, not automatically. Batch payments to align with your weekly check run rather than paying each invoice the moment it arrives. This gives you maximum float without damaging vendor relationships.

Control inventory and overhead

Just-in-time ordering reduces the cash tied up in stock sitting on shelves. A retail business carrying 90 days of inventory when 45 days is sufficient has effectively loaned its suppliers money at 0% interest. Clearing slow-moving stock at a discount frees cash immediately and reduces storage costs.

Audit recurring software subscriptions and service contracts quarterly. Most small businesses carry 3–5 subscriptions that no one actively uses. Canceling them does not improve your product. It improves your cash position with zero operational cost.

Use financing tools correctly

A business line of credit works best as a short-term liquidity buffer for predictable timing gaps, not as a rescue mechanism for operational losses. Using a credit line to cover a payroll gap while waiting for a confirmed client payment is sound practice. Using it to fund ongoing losses is a warning sign that the underlying business model needs attention first.

Invoice factoring, where you sell outstanding invoices to a third party at a discount, provides immediate cash but at a cost. It makes sense for businesses with strong receivables and urgent cash needs. It does not make sense as a permanent substitute for faster invoicing.

How to maintain cash flow health over the long term

Sustainable cash flow health comes from systems and habits, not one-time fixes. A weekly review routine is the single most important habit you can build. Set aside 30 minutes every Monday morning to compare last week’s actuals to your forecast, update your 13-week model, and flag any weeks in the next 90 days that fall below your reserve floor.

Monthly, review your CCC components. Is your DSO trending up? That signals a collections problem. Is your DPO shrinking? That means you are paying vendors faster than your terms require, which costs you float. Tracking these numbers monthly turns abstract metrics into a clear picture of where cash is leaking.

Avoid reactive borrowing. Businesses that borrow only when they are already in trouble pay higher rates, accept worse terms, and signal distress to lenders. Businesses that maintain a clean credit line and draw on it predictably build a track record that improves their borrowing position over time.

Separating cash into segmented accounts prevents accidental use of restricted cash earmarked for taxes or payroll. This structural habit removes the temptation and the risk in one move. Many banks allow you to open multiple business checking accounts at no cost. Use that feature.

Pro Tip: Schedule a quarterly “cash flow audit” with your accountant or a fractional CFO. One hour per quarter reviewing your CCC, reserve levels, and forecast accuracy is worth more than any financial software subscription.

Key Takeaways

Effective cash flow management requires consistent measurement, weekly forecasting, and structural habits that prevent cash from being misused or delayed.

| Point | Details |

|---|---|

| CCC is your core metric | Track Days Sales Outstanding, Days Inventory Outstanding, and Days Payable Outstanding weekly to measure cash health. |

| Use a 13-week rolling forecast | Update your forecast every week to catch shortfalls 60–90 days before they become crises. |

| Invoice fast, collect faster | Send invoices the same day work is complete and shorten payment terms to reduce Days Sales Outstanding. |

| Segment your cash accounts | Keep separate accounts for operations, taxes, and contingencies to prevent spending earmarked funds. |

| Maintain your cash reserve floor | Hold at least 8 weeks of fixed expenses in reserve; seasonal businesses need 12–16 weeks. |

Cash flow is a discipline, not a dashboard

Most small business owners I work with treat cash flow as something they check when things feel tight. That reactive approach is exactly why 82% of business failures link back to cash problems rather than bad products or weak markets. The business was often fine on paper. The cash just ran out before the revenue caught up.

The shift that changes everything is treating your weekly cash review as non-negotiable, the same way you treat payroll. Not because something is wrong, but because staying 60–90 days ahead of a problem is infinitely cheaper than solving it in real time. I have seen businesses with strong revenue and loyal customers collapse in 90 days because they ignored a slow-building receivables problem until it was too late.

The other insight that rarely makes it into generic advice: your vendors and clients are more flexible than you think. Most payment terms are set by default, not by policy. A direct, professional conversation about extending terms or accelerating payment often works on the first ask. You are not begging. You are managing your business like a CFO would.

Cash flow is not a back-office function. It is a competitive advantage. Businesses with strong liquidity can take on larger contracts, negotiate better supplier pricing, and weather slow months without panic. Build the system, run the weekly review, and protect your reserve floor. Everything else follows.

— Black Flame Digital

Put faster invoicing to work for your cash flow

The fastest way to improve your cash position is to get paid sooner. That starts with sending professional invoices the moment work is complete, not at the end of the week or month.

Invoicelabs lets you create and send a professional invoice in under 30 seconds, with real-time tax calculations and instant delivery built in. You can track invoice status, collect payment via Stripe, and maintain consistent branding across every document. Whether you use a free invoice generator for one-off projects or profession-specific templates for consultants and graphic designers, Invoicelabs removes the friction between completing work and collecting cash. Faster invoicing is one of the most direct and immediate cash flow strategies available to any small business.

FAQ

What is a simple cash flow management example?

A cash flow management example is a freelancer who invoices clients on the day of delivery, holds 8 weeks of expenses in a reserve account, and reviews a 13-week forecast every Monday to spot payment gaps before they become problems.

How does the cash conversion cycle affect cash flow?

The cash conversion cycle measures how long it takes to turn work or inventory into collected cash. Shortening it by just 5 days on a $5 million revenue business frees roughly $68,000 in permanent liquidity.

What is the recommended cash reserve for a small business?

Most small businesses should hold 8 weeks of fixed operating expenses in reserve. Seasonal businesses need 12–16 weeks to cover slow periods without disrupting operations.

How often should I update my cash flow forecast?

Update your forecast weekly. A weekly 30-minute review of actuals versus forecast gives you 60–90 days of early warning on cash shortfalls, which is enough time to act without panic.

What is the fastest way to improve cash flow immediately?

Invoice immediately after completing work and shorten your payment terms from Net-30 to Net-15. Simultaneously, negotiate longer terms with suppliers to extend your payables window and keep more cash in your account longer.

Recommended

Send your next invoice in seconds

Create professional invoices, track payments and get paid faster — free to start.